Take a look at your favorite VC’s website. No, I’m serious. Do it right now. I’ll wait.

You’ll probably see some great marketing copy about how out of the box they are, how forward-thinking they are, how they only invest in big ideas, etc. Some of my favorites:

“We believe before others understand.”

“We seed trailblazers, changemakers, and legends in the making.”

“We back visionary founders who are building technologies of the future.”

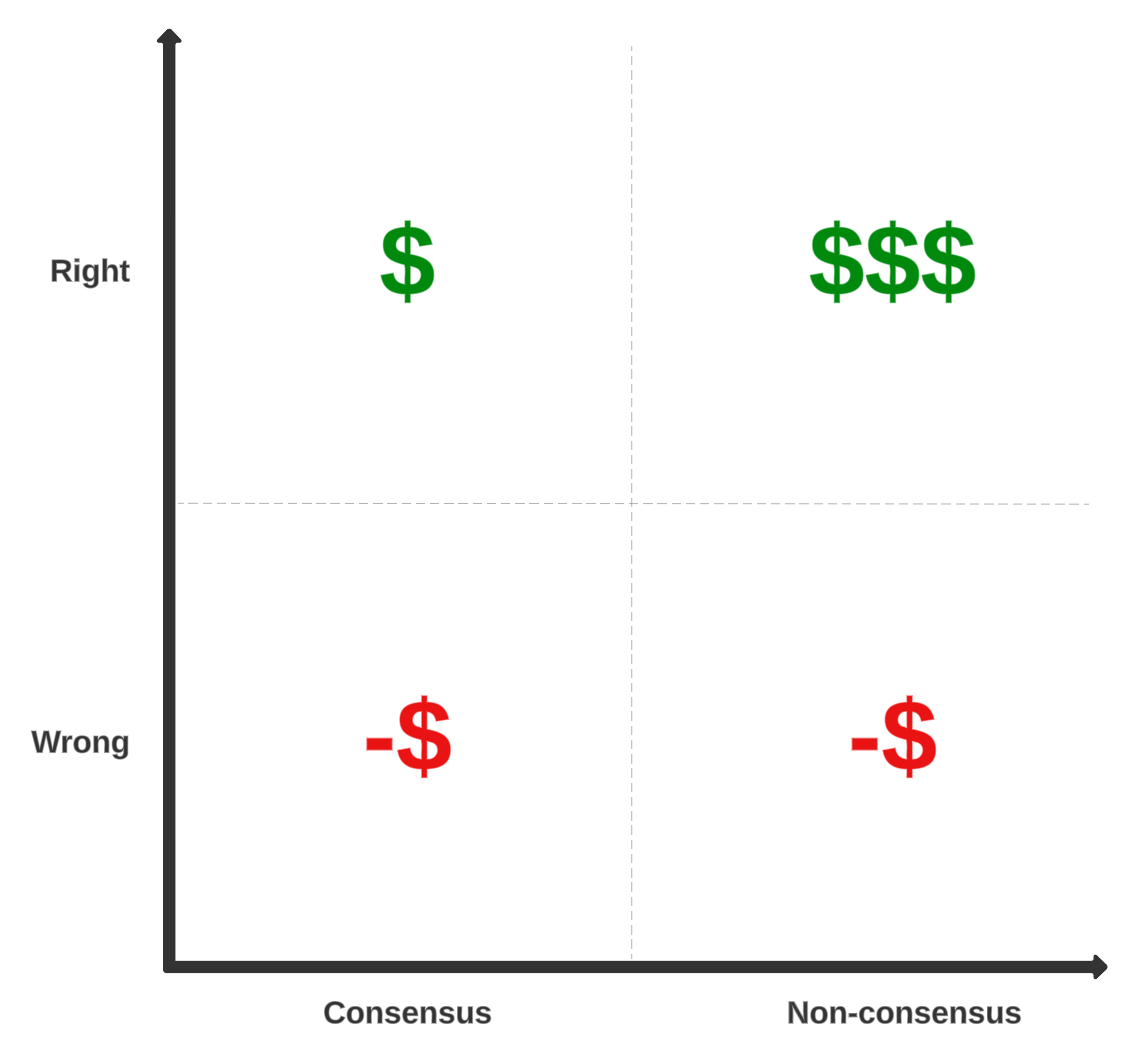

Many venture capitalists talk about being “non-consensus” investors. They may even draw you a neat 2×2 matrix (assuming they’ve been to business school) to demonstrate their point.

You may have seen this before, but let’s do a quick recap of what it means.

If you invest in a “wrong” company (wrong team, wrong product, or wrong market) you’re likely going to lose money. If you invest in a “right” company (right team, right product, and right market) you’re likely going to make money. Pretty simple.

If you believe a company is a “right” company, and lots of other people also believe it is a “right” company, you’re making a consensus bet, and you’ll be able to invest at a price that the broader market believes the company should be valued at, which is probably fair. Assuming it’s actually a “right” company, you’ll all make a little money.

If you believe a company is a “right” company, but everyone else believes it’s a “wrong” company, that’s a non-consensus bet, and you’ll be able to invest at a lower price than if it was a consensus bet. Assuming it’s actually a “right” company, people will eventually learn that it was actually a “right” company all along, and because you bought in at a lower price, you’ll make a LOT more money than if you had invested in a consensus bet.

You can make good money by making consensus bets. But in venture capital, where the power law reigns supreme, investors are incentivized to look for outlier returns, which oftentimes means investing in companies that they believe are “right” but most people believe are “wrong”.

So if early-stage VCs are all about non-consensus bets, why are they notorious for jumping on bandwagons? Why do they care so damn much about who else you may or may not be talking to, and why do they all invest in AI [or insert latest trend if you’re reading this after 2024]? That’s not very “non-consensus” of them, is it?! Why is this?

It’s because non-consensus companies eventually need to turn into consensus companies for VCs to make money. If it stays non-consensus, that by definition means that nobody else believes it’s a “right” company, meaning it’s very hard for founders to raise the capital needed to build a great business. Now, if it really is a “right” company, even if it is a non-consensus bet, it will eventually become a consensus bet. The team will chug along, building and selling product, until one day people will look over and say “oh wow, that is a right company” and buy their stock.

BUT, there’s actually a third axis to our little consensus vs. non-consensus matrix: time. This is where things can get frustrating. A company can be a “right” company if it has the right team, the right product, and the right market. But investors also want the company to grow and become consensus “right” after they invest (or at least before the next fundraise). In most circumstances, investors don’t like to wait 3-5 years for a company to become consensus for a couple of reasons. First, consensus companies attract more investment dollars which means they can hire better and grow faster. Second, investors can show LPs “hey look, I pick ‘right’ companies” sooner which makes it easier for them to raise their next fund. Third, it helps a fund’s IRR. A 3x venture fund in 10 years is stellar. If you push out returns by just 3 years on that same 3x fund to make a 13 year fund, the IRR is cut down by nearly 1/3!

This is why I think “non-consensus” is a bad descriptor. What we are really looking for is “pre-consensus”. Investors don’t want to invest in a non-consensus company, that’s absurd! They just want to invest in a company that isn’t consensus quite yet. It’s going to be consensus in 5 years? No way. Next quarter? I’m in. I think there’s a lot of people who, if given a decade to compound, have the capability to build good teams who will create good products in good markets. But unfortunately, VCs don’t have 15-20 years to let their money cook. This is why the phrase “being early is the same as being wrong” is a thing.

And investing in a pre-consensus company is hard! It takes a lot of research, in-depth understanding, and willingness to accept huge amounts of risk. A big chunk of this is fully understanding the reasons why other investors have passed, and then having a strong conviction that they missed a key detail that you didn’t, they viewed something incorrectly that you see correctly, or they don’t have all the relevant information that you do. You also have to believe that if given the opportunity, the company will be able to mitigate these risks and prove those investors wrong in the next 12-24 months. But coming up with an intellectually sound argument is mentally exhausting and time intensive. Which is why many VCs resort to becoming consensus investors. Just like how nobody gets fired for buying IBM or hiring McKinsey, no GP gets yelled at by their LPs for co-investing with Sequoia.